Forex and Cryptocurrency Forecast for 08 – 12 July 2024

EUR/USD: The US is Not Very Good, Europe is Not Very Bad

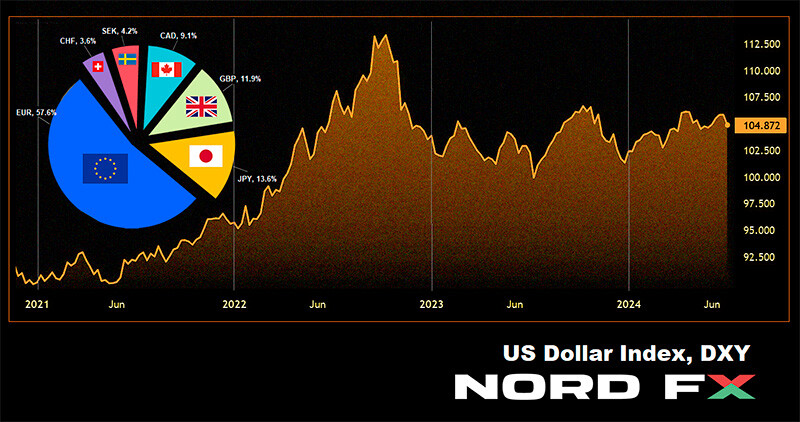

On Friday, June 5, the Dollar Index (DXY) hit a three-week low, while the euro showed its largest weekly gain against the dollar in a year. This was due to the US not performing as well as expected and Europe not faring as poorly.

Disappointing private sector employment statistics from ADP (150K versus the forecasted 163K and previous 157K) and an increase in repeated jobless claims (238K versus 234K) for the ninth consecutive week indicate a cooling labour market. The slowdown in business activity in the service sector, the fastest in four years, and the drop in the ISM Index from 53.8 to 48.8 points, below the threshold of 50.00, suggest that the US economy is not as smooth as the Federal Reserve (Fed) would like.

The FOMC's June meeting minutes mentioned that monetary policy should be ready to respond to economic issues, a sentiment echoed by Fed Chairman Jerome Powell. Consequently, this gloomy macroeconomic data increased the likelihood of a monetary expansion cycle and interest rate cuts in September from 63% to 73%. Derivatives are almost certain that there will be two 25 basis point (bp) cuts in 2024, lowering the rate from 5.50% to 5.00%. This caused US Treasury yields and the DXY to drop, while stock indices and EUR/USD rose. The S&P500 set its 33rd record this year, and EUR/USD reached a high of 1.0842 on July 5.

The euro was also bolstered by the situation in France. The left-wing "New People's Front" (NFP) and the government bloc "Together for the Republic" (Ensemble) joined forces to prevent the right-wing from gaining power, which might end successfully. If the right-wing "National Rally" (RN) does not gain an absolute majority in the new parliament after the second round of elections, there will be no confrontation with the EU or Frexit (analogy with British Brexit).

Polls indicate the right-wing will secure 190 to 250 out of 577 seats, while 289 are needed for an absolute majority. The second round of elections will be held on Sunday, July 7, which might cause gaps in euro pairs on Monday.

Last week, the euro was also supported by the European Central Bank, or rather, by the minutes of its June Governing Council meeting. On one hand, 25 out of 26 Council members voted for a 25 basis point rate cut. However, this decision was made with several caveats concerning still high wage growth rates and the persistence of inflation, which resists and does not want to drop to the target level of 2.0%.

Preliminary June data showed that the CPI decreased only by 0.1% from 2.6% to 2.5%, and the Core CPI remained at 2.9% (y/y), above the consensus forecast of 2.8%. ECB officials fear the CPI might rise due to geopolitical tensions, supply chain disruptions, raw material and energy price increases, and other factors. This almost rules out a rate cut at the ECB Governing Council meeting on July 18 and suggests only one act of monetary expansion in the second half of 2024.

Key US labour market data released at the end of the week on Friday, July 5, could change the dollar's position and the EUR/USD dynamics. According to the Bureau of Labour Statistics (BLS), non-farm payrolls (NFP) increased by 206K in June, lower than May's 218K but above the forecast of 190K. Other data showed the unemployment rate rose from 4.0% to 4.1%, and wage inflation dropped from 4.1% to 3.9% (y/y).

After the publication of this data, EUR/USD ended the week at 1.0839. However, this does not mean it will start the next week at this level. Traders are closely watching the French elections and the political situation related to the November US presidential elections. Biden's interview with ABC News at 00:00 GMT on Saturday, July 6, when markets are closed, could also impact dollar pairs.

As of the evening of July 5, analysts' forecasts for the near future are as follows: 55% predict the pair will rise, 45% foresee a fall. In technical analysis, all trend indicators and oscillators on D1 are in favour of the euro, although a quarter indicate the pair is overbought. The nearest support is in the 10790-10805 zone, followed by 1.0725, 1.0665-1.0680, 1.0600-1.0620, 1.0565, 1.0495-1.0515, 1.0450, and 1.0370. Resistance zones are at 1.0890-1.0915, 1.0945, 1.0980-1.1010, 1.1050, and 1.1100-1.1140.

Notable events in the upcoming week include Jerome Powell's testimony in the US Congress on July 9 and 10, updated CPI data for Germany and the US on Thursday, July 11, and US initial jobless claims. The week will end with Germany's retail sales data and the US Producer Price Index (PPI) and the University of Michigan Consumer Sentiment Index.

GBP/USD: The Pound Gained with the Labour Party

The pound sterling and British stocks rose after the opposition centre-left Labour Party secured a convincing victory in the parliamentary elections. The British currency achieved a weekly gain of 1% – the best in the last seven weeks.

According to Reuters, the Labour Party won 337 out of 650 seats, indicating a majority in the House of Commons. UK Prime Minister Rishi Sunak conceded defeat and congratulated his opponents on their victory. In turn, Labour Party leader and Prime Minister-elect Keir Starmer declared that from today "we are embarking on a mission of national renewal and starting to rebuild our country." Starmer will replace Sunak as Prime Minister, ending 14 years of Conservative rule.

The markets responded positively to the national election results. The pound became the only component of the DXY to strengthen (by 0.2%) this year. "Apart from the weakening of the dollar," commented Singapore's DBS Bank, "the markets warmly welcomed the victory of the opposition Labour Party. This will put an end to years of political and economic uncertainty under Conservative leadership following the Brexit referendum in 2016. Labour leader Keir Starmer, while he is alive, has ruled out the possibility of the UK joining three blocs – the EU, the single market, and the customs union. […] However, Labour may seek more favourable trade agreements by aligning with EU rules in specific sectors such as agriculture, food, and chemicals."

"As for monetary policy," continued DBS strategists, "the OIS market assesses a 62.4% probability of the Bank of England (BoE) cutting the rate by 25 basis points to 5.0% at the meeting on August 1." However, DBS believes this will not significantly harm the pound, provided that expectations for a Fed rate cut in September increase.

The final note of the five-day period saw the GBP/USD pair at 1.2814. Specialists from another Singaporean bank, UOB, believe the likelihood of the pound strengthening has increased. They note that a strong resistance level is in the area of last month's high of 1.2860. The median forecast for the near term is as follows: 35% of analysts expect further pound strengthening and pair growth, 50% foresee a decline, and the remaining 15% are neutral. As for technical analysis on D1, 100% of trend indicators are green. Among the oscillators, 90% are green, a third of which are in the overbought zone, and the remaining 10% are neutral grey. In case of further decline, the pair will find support levels and zones at 1.2735-1.2750, 1.2680, 1.2655, 1.2610-1.2625, 1.2540, 1.2445-1.2465, 1.2405, and 1.2300-1.2330. In case of growth, the pair will meet resistance at levels 1.2850-1.2860, followed by 1.2895, 1.2965-1.2995, 1.3040, and 1.3130-1.3140.

Among the events of the coming week, the publication of UK GDP data for May on Thursday, July 11, stands out. The next important event, as previously mentioned, will be the publication of a fresh inflation report in the United Kingdom on July 17.

continued below...