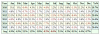

I have created a trading system and I wanted to know from the other algo traders on the community what they think of the results and what are the odds of it holding true in a real trading environment.

For the trades I have assumed that they are executed on the open of the next candle and stop losses are hit intraday and commissions and slippages all inclusive are assumed at 0.035% per trade.

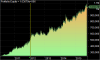

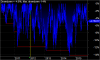

The attached results are on bank nifty for nifty I get a CAGR of 18% (for the same period) and a max drawdown of 11.5%.

Would really appreciate if some people could share their inputs on the motecarlo simulation and their defination of a robust system

For the trades I have assumed that they are executed on the open of the next candle and stop losses are hit intraday and commissions and slippages all inclusive are assumed at 0.035% per trade.

The attached results are on bank nifty for nifty I get a CAGR of 18% (for the same period) and a max drawdown of 11.5%.

Would really appreciate if some people could share their inputs on the motecarlo simulation and their defination of a robust system

Attachments

-

41.6 KB Views: 574

41.6 KB Views: 574 -

11.8 KB Views: 568

11.8 KB Views: 568 -

14.7 KB Views: 561

14.7 KB Views: 561 -

16.7 KB Views: 569

16.7 KB Views: 569 -

20.3 KB Views: 570

20.3 KB Views: 570

Last edited:

")